Bank Of America, Broker Back Revival Of Subprime Mortgage Market

Fahad Shabbir (@FahadShabbir) Published October 22, 2018 | 09:35 PM

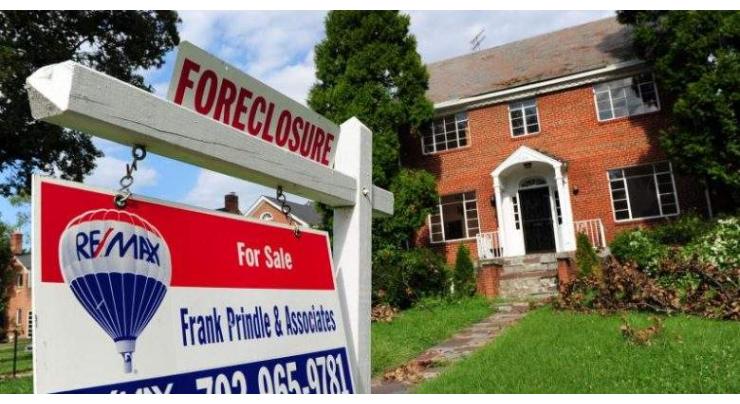

A decade after the subprime mortgage crisis, thousands of potential home buyers with poor credit are lining up for zero down, low interest home loans backed by one of the biggest banks in the business.

NEw YORK, (UrduPoint / Pakistan Point News - 22nd Oct, 2018 ) :A decade after the subprime mortgage crisis, thousands of potential home buyers with poor credit are lining up for zero down, low interest home loans backed by one of the biggest banks in the business.

Throughout this year, Bank of America and Boston-based non-profit brokerage Neighborhood Assistance Corporation of America are holding events nationwide offering mortgages to low and moderate income people and minority home buyers.

Specifically, the groups are offering the loans to buyers with poor or rehabbing credit, which was one of the issues that contributed to the last meltdown -- buyers who couldn't afford the mortgages they had.

Bank of America and NACA, though, say they have a vetting system in place to help prospective home buyers who shouldn't be excluded by credit score alone.

NACA CEO Bruce Marks told UPI the organization has been working with Bank of America since the early 1990s when then-CEO Hugh McColl agreed to commit $1.5 billion in mortgage commitments after reviewing the program, a number that's grown to $10 billion today.

We've been satisfied with how NACA has been able to educate home buyers and the loans that NACA brings us, Bank of America spokesman Terry Francisco told UPI. The borrowers that NACA brings us have performed well over the nearly 20 years we've been involved with them.

Marks hailed the mortgages offered through the program as the best in America, touting no foreclosures on loans distributed over the last six years.

After the subprime lending market had largely cooled in the years following the housing crisis of the early 2000s, banks have slowly begun making these kinds of loans again with a greater focus on ensuring they can be repaid.

The definition of a subprime loan has changed. What we're calling a subprime loan today, there's probably a fair amount of overlap between what we called subprime loans in 2006, but some of the practices from 2006 like the no documentation, no income verification loan are not really happening at the same rate as they were before, NYU Asst. Professor of Sociology and Public Service Jacob Faber told UPI.

Character-based lending NACA and Bank of America offer 15- or 30-year fixed loans with interest rates below market average, coming in at about 4.5 percent. They also offer no-down payment, no closing costs, no fees and no requirement for a credit score to initiate the loan.

Rather than focusing on a borrower's credit score, Marks said NACA engages in character-based lending.

"We don't consider people's credit score, we look at their payment history that they control. So that means that if someone has a low credit score because they're late on their medical bills and they can't control it because they have to go to the emergency room or things out of their control, we don't consider that," Marks said.

Borrowers are then required to provide full documentation including bank statements, W-2 forms, tax returns and other information to construct a comprehensive budget that is used to determine the borrower's mortgage payment will be.

"We base their payment on both their budget and what they pay in rent that they can afford," Marks said.

One way NACA ensures that potential home buyers can afford the mortgage is demonstrating they can handlethe payment shock -- the difference between what they're paying now and what they will pay with the newmortgage.

Recent Stories

Non-Muslim Pakistanis enjoy freedom, state patronage: Kundi

10 minutes ago

Dengue Control Committee gathers in Jhang

10 minutes ago

BHP launches $38.8 billion takeover bid for rival Anglo American

10 minutes ago

Saudi oil giant Aramco agrees major FIFA sponsorship deal

10 minutes ago

Awais Leghari meets Chief Minister Sindh

10 minutes ago

Putin says plans to visit China in May

10 minutes ago

IHC adjourns cipher case till April 30

10 minutes ago

Identification specifics required to know about lawmakers put on travel stop lis ..

10 minutes ago

Court stops PTI founder, his wife from provocative statements against institutio ..

10 minutes ago

Experts demand stakeholder intervention to boost tax-net, revitalize taxation re ..

9 minutes ago

Higher taxes, awareness help decrease cigarettes sale in Pakistan

35 minutes ago

Sindh Minister of Works and Services Ali Hassan Zardari reviews ongoing projects ..

38 minutes ago

More Stories From Business

-

Higher taxes, awareness help decrease cigarettes sale in Pakistan

35 minutes ago -

Ahsan Iqbal chairs CPEC JWGs, 13th JCC review-meeting

38 minutes ago -

Industries Minister recommends urea fertilizer import to stabilize prices and supply

38 minutes ago -

Honda announces US$11 bn EV battery and vehicle plant in Canada

38 minutes ago -

Zhao Shirin calls on Punjab Industries Minister

1 hour ago -

CEO APM Terminals calls on Finance Minister

1 hour ago

-

SACM visits GTVC checks attendance register

1 hour ago -

CEO APM Terminals meets Commerce Minister

1 hour ago -

RTO destroys huge quantity of non-duty paid cigarettes

2 hours ago -

Pakistan's total liquid foreign reserves reach $ 13.28 billion

2 hours ago -

RDA inflows rise to $7.660 bn in March 24

2 hours ago -

FPCCI welcomes direct flights between Pakistan-Azerbaijan

2 hours ago